Why AML is a Critical Control Point for Regulated Small Businesses

Anti-Money Laundering (AML) Requirements:

In the UAE, Anti-Money Laundering (AML) requirements do not apply equally to all businesses. They apply to specific sectors—designated non-financial businesses and professions (DNFBPs), financial services activities, and other regulated categories that involve exposure to financial transactions, client funds, or high-value assets.

If your business falls into one of these categories, AML is not optional.

It is a core operating requirement from day one.

For small business owners in these sectors, the challenge is not whether AML applies, but how to implement it correctly—while still focusing on customers, revenue, and execution.

At the start, most businesses take action. Documentation is prepared. Risk assessments are completed. Submissions are made. This reflects awareness of the requirement.

But AML is not defined by activity.

It is defined by structure.

This is where the distinction begins. Two businesses in the same regulated category may complete similar requirements, yet only one is operating under control. The difference is not effort. It is a measure of how well the system behind that effort is designed.

Who This Applies To

AML obligations apply to businesses operating in sectors where financial exposure, transaction flow, or asset movement creates regulatory risk. This typically includes:

- Real estate brokers and agents.

- Corporate service providers.

- Accounting and audit firms.

- Dealers in precious metals and stones.

- Certain consulting and advisory businesses handle financial structuring or client funds.

In these sectors, AML is part of how the business is expected to operate—not an additional layer applied later.

The expectation is clear.

You understand your risk.

You document it properly.

You can demonstrate control.

What Good AML Actually Looks Like

For many small business owners, AML remains abstract. It is understood as a requirement, but not always as a working system. In practice, well-structured AML is clear, consistent, and repeatable.

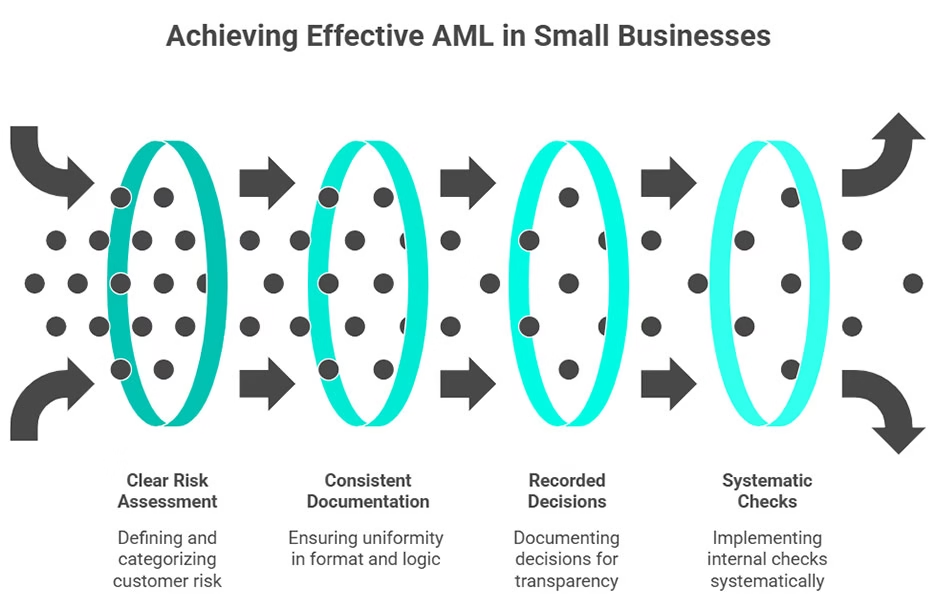

The business knows exactly how customer risk is assessed and categorized. Documentation is not just present, but aligned—consistent in format, logic, and depth. Decisions are recorded in a way that can be explained, both internally and externally. Internal checks are defined and applied systematically, rather than relying on individual judgment.

There is no ambiguity around what has been done or why.

This is what regulators expect to see.

Not complexity.

Not volume.

Clarity.

A business operating with strong AML does not need to reconstruct its position under review. It can demonstrate it immediately, because the structure already exists.

Moving Beyond Completion to Control

In regulated sectors, AML is often treated as an add-on to other operational priorities. This creates progress, but not always control.

Control comes from alignment.

When documentation reflects the business’s actual activities. When risk assessments are tailored to the specific sector, client profile, and transaction types involved. When internal processes ensure that what is submitted has been reviewed, checked, and validated before it reaches an external authority.

At that point, AML moves from being a compliance obligation to being part of how the business operates.

It becomes embedded.

This is where the shift occurs—from compliance to management.

Why Structure Matters Early in Regulated Sectors

For businesses operating in AML-relevant sectors, there is no transitional period where informal approaches are sufficient. Regulatory expectations apply immediately and consistently.

This does not require complexity.

It requires accuracy.

A business that defines its AML approach from day one avoids rework later. Documentation does not need to be revisited or corrected. Risk assessments do not need to be reinterpreted. Processes do not need to be introduced under pressure.

Instead, the business operates under a system already aligned with its regulatory obligations.

This creates stability.

It also ensures that compliance does not disrupt the business as it grows.

The Role of Expertise in Regulated Environments

For most small business owners, AML is not a core capability. Yet in regulated sectors, the standard expected is precise.

This creates a gap.

Not in awareness—but in execution.

Time is often spent interpreting regulatory guidance, understanding sector-specific requirements, and refining documentation. But without a defined methodology, this effort does not always translate into confidence.

- Expert support provides structure.

- A clear interpretation of how AML applies to your specific business type.

- A defined approach to risk assessment based on your sector and client profile.

- Documentation aligned to regulatory expectations from the outset.

- Guidance on how to manage authority communication effectively.

This ensures that compliance is not generic.

It is specific, relevant, and defensible.

Building a System That Holds Under Review

AML is ultimately tested under review.

For regulated businesses, this is where the system’s quality becomes evident.

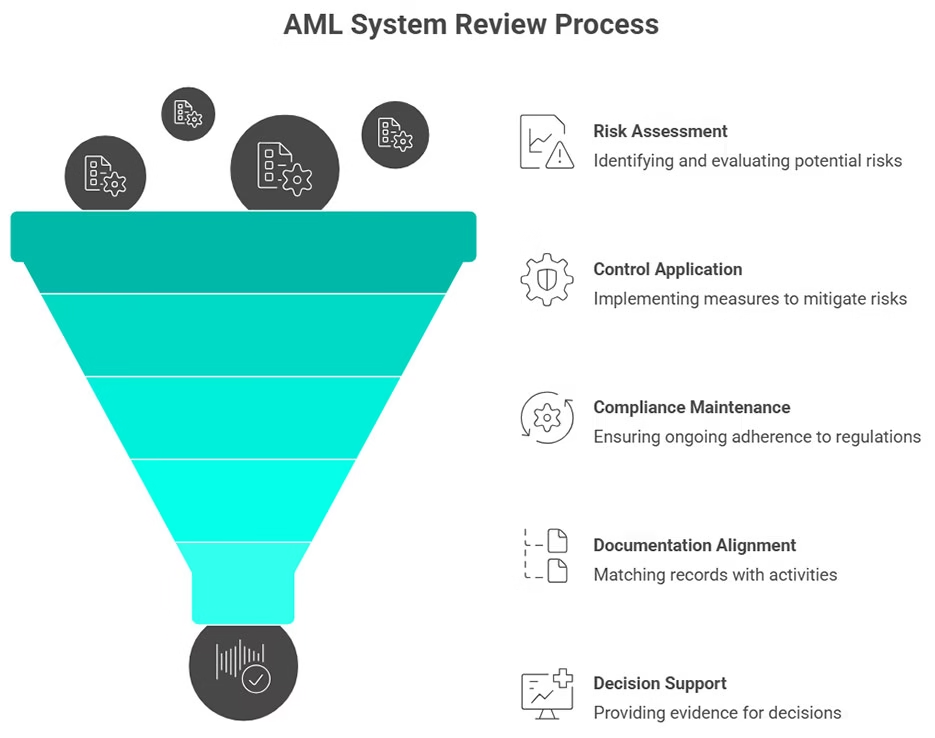

A well-prepared business can clearly demonstrate how risk has been assessed, how controls have been applied, and how compliance has been maintained over time. Documentation aligns with the activity. Decisions are supported. Processes are consistent.

Everything connects.

This is what regulators expect to see from businesses operating in AML-relevant sectors.

Not just that, the requirements have been completed.

But the system behind them is sound.

A Practical Approach for Small Businesses in AML-Regulated Sectors

For small businesses, the objective is not to replicate a large-scale compliance function. It is to ensure that the fundamentals are correct, proportionate, and aligned to the specific risks of the business.

- This requires a focused approach.

- Define obligations based on your sector.

- Align documentation to those obligations.

- Build risk assessments around actual client and transaction profiles.

- Introduce clear internal checks.

- Ensure submissions are consistent, accurate, and complete.

When these elements are in place, AML becomes manageable.

More importantly, it becomes reliable.

From Compliance Activity to Operational Confidence

The shift is not about doing more.

It is about doing it correctly.

From generic compliance to sector-specific alignment.

From fragmented effort to structured execution.

From uncertainty to clarity.

This is what allows regulated businesses to operate with confidence—not only in meeting requirements, but in knowing that their approach will hold under scrutiny.

Conclusion

AML does not apply to every business, but for those it does apply to, it is fundamental.

It is not an add-on.

It is not a secondary consideration.

It is part of how the business must operate.

For small business owners in regulated sectors, the question is not whether AML has been completed.

It is whether it has been implemented in a way that reflects the specific risks, requirements, and expectations of their industry.

Businesses that get this right early operate with clarity and control. Those who do not often find themselves having to revisit and restructure their approach under pressure.

The most effective path is to build the right system from the outset—aligned with the business, supported by expertise, and designed to withstand review.

That is where partners like EZONE come in.

Book a Consultation

Fill out the form in the sidebar, and we’ll arrange a time that works for you.